“We … join the other circuits in holding that consumer reporting agencies are not

required to investigate the legal validity of disputed debts under the FCRA.” Reyes v. Equifax, No. 24-40415 (June 13, 2025).

Category Archives: Consumer

In Calogero v. Shows, Cali & Walsh, LLP, (discussed earlier this week for stylistic reasons), a panel majority found that two recipients of certain Hurricane Katrina relief stated a viable Fair Debt Collection Act claim when:

- The longest possible limitations period (10 years) had run by the time the demand letters requested payment; and

- The demand letters threatened a claim for attorneys fees, when the relevant documents only created a specific right to potential fee recovery that did not include the alleged debt at issue.

The third judge, without opinion, concurred in the result only. No. 22-30487 (March 15, 2024).

The plaintiff in Fontana v. H O V G L L C alleged that a debt collector violated the Fair Debt Collection Act by speaking with his sister. His claim failed because the FDCA requires a “communication,” and in this case: “[T]he conversation between HOVG’s representative and Fontana’s sister did not convey any information regarding a debt, either directly or indirectly. HOVG’s representative did not mention Fontana’s debt at all and did not directly provide any information about it. Instead, HOVG’s representative mentioned ‘an important personal business matter.’ That does not even suggest the existence of a debt, much less provide information about it. The closest HOVG’s representative came to giving information about a debt was providing the name of the debt collector.” No. 20-30471 (Feb. 26, 2021).

Manuel owed $250 to an orthopedics practice, first billed in December 2010 and January 2011. Merchants Professional, a collection agency, sent him “six collection

Manuel owed $250 to an orthopedics practice, first billed in December 2010 and January 2011. Merchants Professional, a collection agency, sent him “six collection

letters in 2011 and, after six years with seemingly no collection effort, it sent

four more in 2017.” Manuel sued for violation of the FDCPA arguing that it was improper to seek collection of a debt after the limitations period had run.

The Fifth Circuit reviewed and sidestepped earlier precedent which suggested that attempts to collect time-barred debt were per se violations of the Act. It nevertheless affirmed judgment for Manuel based on the specific contents of these letters, holding that “these letters seeking collection of time-barred debt, filled with ambiguous offers and threats with no indication that the debt is old, much less that the limitations period has run, misrepresent the legal enforceability of the underlying debt . . . .” Manuel v. Merchants & Professional Bureau, No. 19-50814 (April 29, 2020) (emphasis added).

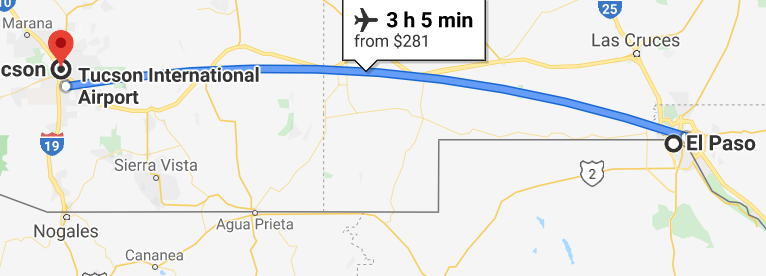

Rogers, a collection agency, wrote Salinas, stating the amount due ($4629.96)

and the interest and fees due ($0.00). The letter also said: “In the event there is interest or other charges accruing on your account, the amount due may be greater than the  amount shown above after the date of this notice.”

amount shown above after the date of this notice.”

The Fifth Circuit held that, while its precedent had not squarely addressed “conditional” language such as “in the event,” Rogers’s letter was not deceptive. “Salinas reads it to imply the possibility that interest or other charges may accrue when in fact they cannot,” noted the Court, but “[a]n illustration shows the problem with Salinas’ reading of the letter”:

Suppose a traveler boards a flight from El Paso, TX, to Tucson, AZ—a route traversing only desert—and is shown a safety video describing steps to take “in the event of a water landing.” Even the least sophisticated traveler would not take the video to imply the plane would be flying over water. No passenger would leap out of his seat in panic, concluding he had boarded the wrong flight. Even a traveler “tied to the very last rung on the intelligence or sophistication ladder” would interpret the video as merely acknowledging the reality that some flights, if not this one, fly over water.

Salinas v. R.A. Rogers Inc., No. 19-50618 (March 12, 2020).

The Consumer Financial Protection Bureau – the subject of ongoing litigation about the constitutionality of its structure, which has been at issue in the recent Kavanaugh hearings – lost a challenge to a civil investigative demand in CFPB v. The Source for Public Data: “The CFPB did not comply with 12 U.S.C. § 5562(c)(2) when it issued this CID to Public Data. First, it did not state the ‘conduct constituting the alleged violation which is under investigation.’ According to its Notification of Purpose, the CFPB is investigating ‘unlawful acts and practices in connection with the provision or use of public records information.’ Simply put, this Notification of Purpose does not identify what conduct, it believes, constitutes an alleged violation. . . . Moreover, this CID does not identify ‘the provision of law applicable to such violation.’ As discussed, the CID never identifies an alleged violation, so it is unsurprising that it fails to identify a relevant provision of law.” No. 17-10732 (Sept. 6, 2018).

The Consumer Financial Protection Bureau – the subject of ongoing litigation about the constitutionality of its structure, which has been at issue in the recent Kavanaugh hearings – lost a challenge to a civil investigative demand in CFPB v. The Source for Public Data: “The CFPB did not comply with 12 U.S.C. § 5562(c)(2) when it issued this CID to Public Data. First, it did not state the ‘conduct constituting the alleged violation which is under investigation.’ According to its Notification of Purpose, the CFPB is investigating ‘unlawful acts and practices in connection with the provision or use of public records information.’ Simply put, this Notification of Purpose does not identify what conduct, it believes, constitutes an alleged violation. . . . Moreover, this CID does not identify ‘the provision of law applicable to such violation.’ As discussed, the CID never identifies an alleged violation, so it is unsurprising that it fails to identify a relevant provision of law.” No. 17-10732 (Sept. 6, 2018).

Before a lender may accelerate a debt (and later foreclose), Texas law requires that the lender send (1) notice of intent to accelerate, followed by (2) notice of acceleration. While “Texas courts have not squarely confronted whether a borrower is entitled to a new round of notice when a borrower re-accelerates following an earlier rescission,” the Fifth Circuit concluded “that the Texas Supreme Court would require such notice . . . Abandonment of acceleration ‘restor[es] the contract to its original condition.’ The Texas Supreme Court would likely conclude that Wilmington Trust acted ‘inconsistently’ by rescinding acceleration and then re-accelerating without notice.” Wilmington Trust v. Rob, No. 17-50115 (May 21, 2018).

Before a lender may accelerate a debt (and later foreclose), Texas law requires that the lender send (1) notice of intent to accelerate, followed by (2) notice of acceleration. While “Texas courts have not squarely confronted whether a borrower is entitled to a new round of notice when a borrower re-accelerates following an earlier rescission,” the Fifth Circuit concluded “that the Texas Supreme Court would require such notice . . . Abandonment of acceleration ‘restor[es] the contract to its original condition.’ The Texas Supreme Court would likely conclude that Wilmington Trust acted ‘inconsistently’ by rescinding acceleration and then re-accelerating without notice.” Wilmington Trust v. Rob, No. 17-50115 (May 21, 2018).

The question in Peake v. Ayobami was whether a bankruptcy debtor, who asserts a 100% exemption as to a particular estate asset, is asserting that exemption as to the asset itself or its value. The practical consequence is whether “claiming a 100% interest in an asset as exempt allows the debtor to ‘walk away’ with the asset itself and potentially benefit from any post-petition appreciation of it.” The Fifth Circuit gave a limited answer, noting that the statute allows the debtor to claim “a 100% interest in an asset,” and also noting Supreme Court precedent that expressed skepticism about whether a debtor could use this ability to get clear title to a valuable asset, but not providing an ultimate answer to the question. Ni. 16-20589 (Jan. 3, 2018).

The question in Peake v. Ayobami was whether a bankruptcy debtor, who asserts a 100% exemption as to a particular estate asset, is asserting that exemption as to the asset itself or its value. The practical consequence is whether “claiming a 100% interest in an asset as exempt allows the debtor to ‘walk away’ with the asset itself and potentially benefit from any post-petition appreciation of it.” The Fifth Circuit gave a limited answer, noting that the statute allows the debtor to claim “a 100% interest in an asset,” and also noting Supreme Court precedent that expressed skepticism about whether a debtor could use this ability to get clear title to a valuable asset, but not providing an ultimate answer to the question. Ni. 16-20589 (Jan. 3, 2018).

Tower Credit garnished the debtor’s wages. In defense of a later preference action, Tower argued that its garnishment was effective when served (taking it outside the preference period), not when the debtor in fact received money. The Fifth Circuit disagreed: “The combination of Supreme Court precedent and the overwhelming weight of persuasive authority applying §

Tower Credit garnished the debtor’s wages. In defense of a later preference action, Tower argued that its garnishment was effective when served (taking it outside the preference period), not when the debtor in fact received money. The Fifth Circuit disagreed: “The combination of Supreme Court precedent and the overwhelming weight of persuasive authority applying § ![]() 547(e)(3) make clear that a debtor’s wages cannot be transferred until they are earned. Thus, we hold that a creditor’s collection of garnished wages earned during the preference period is an avoidable transfer made during the preference period even if the garnishment was served prior to that period.” Tower Credit v. Schott, No. 16-30274 (March 13, 2017).

547(e)(3) make clear that a debtor’s wages cannot be transferred until they are earned. Thus, we hold that a creditor’s collection of garnished wages earned during the preference period is an avoidable transfer made during the preference period even if the garnishment was served prior to that period.” Tower Credit v. Schott, No. 16-30274 (March 13, 2017).

![]() Bacharach, upset by the handling of credit reporting by SunTrust, sued it under the FCRA. The Fifth Circuit affirmed summary judgment for SunTrust, noting:

Bacharach, upset by the handling of credit reporting by SunTrust, sued it under the FCRA. The Fifth Circuit affirmed summary judgment for SunTrust, noting:

- Reporting about a failed “flip” of commercial property — especially when the alleged losses involved lost rental income — did not fall within the scope of the FCRA;

- Evidence of other, unrelated payment problems during the relevant period negated the element of causation; and

- “Vague and conclusory deposition testimony” does not establish actionable emotional distress under the FCRA.

Bacharah v. Suntrust Mortgage, No. 15-31009 (June 30, 2016).

Billings v. Propel Financial Services, LLC involved plaintiffs, making claims under the Truth in Lending Act, arising from property tax loans they obtained in exchange for the transfer of their tax liens pursuant to the Texas Tax Code. Applying prior precedent in a an analogous bankruptcy context, the Fifth Circuit held: “[I]t is clear that the payments made by defendants to the relevant taxing authorities and the subsequent transfer of the tax liens and execution of the promissory notes did not extinguish the original tax obligations, but rather, simply transferred the preexisting tax obligations to new entities. Thus, the transfers and promissory notes did not create new debts that would be subject to TILA, but rather transferred existing tax obligations, which are not ‘debts’ subject to TILA.” No. 14-51326-CV (April 29, 2016).

Billings v. Propel Financial Services, LLC involved plaintiffs, making claims under the Truth in Lending Act, arising from property tax loans they obtained in exchange for the transfer of their tax liens pursuant to the Texas Tax Code. Applying prior precedent in a an analogous bankruptcy context, the Fifth Circuit held: “[I]t is clear that the payments made by defendants to the relevant taxing authorities and the subsequent transfer of the tax liens and execution of the promissory notes did not extinguish the original tax obligations, but rather, simply transferred the preexisting tax obligations to new entities. Thus, the transfers and promissory notes did not create new debts that would be subject to TILA, but rather transferred existing tax obligations, which are not ‘debts’ subject to TILA.” No. 14-51326-CV (April 29, 2016).

Appellant “Why Not LLC” (unfortunately, not the appellee, despite the perfect name for that side of an appeal) complained of a frozen yogurt franchise termination by Yumilicious. The district court granted summary judgment on Why Not’s many causes of action, and the Fifth Circuit affirmed, principally on grounds relating to Yumilicious’s lack of intent and the terms of the franchise agreement. In the course of doing so, the opinion offers a primer on commonly-litigated issues about basic business torts in Texas. The Court observed that Why Not’s pleading had presented “a large serving of claims and counterclaims piled precariously together,” and concluded: “This saccharine swirl of counterclaims suggests that litigants, like fro-yo fans, should seek quality over quantity.” Yumilicious v. Barrie, No. 15-10508 (April 6, 2016). (The opinion is silent as to whether Why Not has any relation to the left fielder on Bud Abbott’s famous baseball team.)

Appellant “Why Not LLC” (unfortunately, not the appellee, despite the perfect name for that side of an appeal) complained of a frozen yogurt franchise termination by Yumilicious. The district court granted summary judgment on Why Not’s many causes of action, and the Fifth Circuit affirmed, principally on grounds relating to Yumilicious’s lack of intent and the terms of the franchise agreement. In the course of doing so, the opinion offers a primer on commonly-litigated issues about basic business torts in Texas. The Court observed that Why Not’s pleading had presented “a large serving of claims and counterclaims piled precariously together,” and concluded: “This saccharine swirl of counterclaims suggests that litigants, like fro-yo fans, should seek quality over quantity.” Yumilicious v. Barrie, No. 15-10508 (April 6, 2016). (The opinion is silent as to whether Why Not has any relation to the left fielder on Bud Abbott’s famous baseball team.)

The plaintiffs in Hall v. Phenix Investigations were also defendants in contentious state court fraudulent transfer litigation. They alleged that a private investigation firm violated the FCRA in its work in that litigation. The Fifth Circuit affirmed the dismissal of the case on the pleadings, finding that “the report was commissioned for use in ongoing commercial litigation, which is not a qualifying purpose of the FCRA even it may potentially be used for such a purpose someday. And, “[e]ven assuming that filing a lawsuit to collect on a judgment could constitute the collection of a consumer account within the meaning of the FCRA, there is no collection of a consumer account here because the judgment arose from a commercial transaction.” No. 15-10533 (March 29, 2016, unpublished).

The plaintiffs in Hall v. Phenix Investigations were also defendants in contentious state court fraudulent transfer litigation. They alleged that a private investigation firm violated the FCRA in its work in that litigation. The Fifth Circuit affirmed the dismissal of the case on the pleadings, finding that “the report was commissioned for use in ongoing commercial litigation, which is not a qualifying purpose of the FCRA even it may potentially be used for such a purpose someday. And, “[e]ven assuming that filing a lawsuit to collect on a judgment could constitute the collection of a consumer account within the meaning of the FCRA, there is no collection of a consumer account here because the judgment arose from a commercial transaction.” No. 15-10533 (March 29, 2016, unpublished).

Dixon complained that he was defrauded into leasing a Toyota Corolla, having been told that the lease would be tax-exempt because his co-lessee was a non-profit entity. The Fifth Circuit affirmed dismissal, finding that the Consumer Leasing Act does not confer standing unless all lessees are natural persons, which the non-profit was not. Dixon v. Toyota Motor Credit Corp., No. 14-30426 (July 23, 2015).

Dixon complained that he was defrauded into leasing a Toyota Corolla, having been told that the lease would be tax-exempt because his co-lessee was a non-profit entity. The Fifth Circuit affirmed dismissal, finding that the Consumer Leasing Act does not confer standing unless all lessees are natural persons, which the non-profit was not. Dixon v. Toyota Motor Credit Corp., No. 14-30426 (July 23, 2015).

After completing her Chapter 13 plan, Juliana Jett owed roughly $35,000 on her mortgage, with $0 past due. Her Experian credit report, however, erroneously showed it as discharged with a $0 balance, which Jett alleged caused her to be denied refinancing. She complained to Experian four times, who in turn sent an “automatic credit dispute verification form” to American Home Mortgage Servicing each time. She sued under the Fair Credit Reporting Act, alleging that “[i]n each instance, American Home tried to correct the information but returned a blank [Consumer Information Indicator] field so Experian did not process the updates.” The Fifth Circuit reversed a summary judgment for the servicer as to Jett’s negligence claim, noting that this evidence allowed an inference that “American Home knew that Jett’s information was being reported inaccurately and attempted to correct it.” The adequacy of the servicer’s procedures was an issue to be resolved at trial. Jett v. American Home Mortgage Servicing, Inc., No. 14-10771 (June 10, 2015, unpublished).

After completing her Chapter 13 plan, Juliana Jett owed roughly $35,000 on her mortgage, with $0 past due. Her Experian credit report, however, erroneously showed it as discharged with a $0 balance, which Jett alleged caused her to be denied refinancing. She complained to Experian four times, who in turn sent an “automatic credit dispute verification form” to American Home Mortgage Servicing each time. She sued under the Fair Credit Reporting Act, alleging that “[i]n each instance, American Home tried to correct the information but returned a blank [Consumer Information Indicator] field so Experian did not process the updates.” The Fifth Circuit reversed a summary judgment for the servicer as to Jett’s negligence claim, noting that this evidence allowed an inference that “American Home knew that Jett’s information was being reported inaccurately and attempted to correct it.” The adequacy of the servicer’s procedures was an issue to be resolved at trial. Jett v. American Home Mortgage Servicing, Inc., No. 14-10771 (June 10, 2015, unpublished).

Can a note be endorsed with a photocopied signature? Yes. Whittier v. Ocwen Loan Servicing, LLC, No. 13-20639 (Dec. 3, 2014, unpublished) (citing Tex. Bus. & Com. Code § 1.201(b)(37)) (“Signed” includes using any symbol executed or adopted with present intention to adopt or accept a writing.”)

Can a note be endorsed with a photocopied signature? Yes. Whittier v. Ocwen Loan Servicing, LLC, No. 13-20639 (Dec. 3, 2014, unpublished) (citing Tex. Bus. & Com. Code § 1.201(b)(37)) (“Signed” includes using any symbol executed or adopted with present intention to adopt or accept a writing.”)

Can a “deed of trust . . . upon a homestead exempted from execution,” which “shall not be valid or binding unless signed by the spouse of the owner,” be signed in separate but identical documents? Yes. Avakian v. Citibank, N.A., No. 14-60175 (Dec. 9, 2014) (citing Duncan v. Moore, 7 So. 221, 221-22 (Miss. 1890)) (“There is much force in the  argument of defendant’s counsel that the statute does not require a joint deed of husband and wife for the conveyance of the husband’s homestead . . . that the substantial thing is the written evidence of such consent; and that this may be as certainly shown by a separate instrument as by signing the deed of the husband.”)

argument of defendant’s counsel that the statute does not require a joint deed of husband and wife for the conveyance of the husband’s homestead . . . that the substantial thing is the written evidence of such consent; and that this may be as certainly shown by a separate instrument as by signing the deed of the husband.”)

Mabary withdrew money from an A TM machine. While she received an on-screen notice about a $2.00 fee, the machine did not have a posted external notice about the fee — a violation of the Electronic Funds Transfer Act at the time. After amendments to the EFTA that eliminated the Bank’s liability (if applicable), the district court dismissed Mabary’s claim and denied certification of a related class. Mabary v. Home Town Bank, N.A., No. 13-20211 (Nov. 5, 2014). The Fifth Circuit reversed, holding: (1) Mabary had Article III standing as a result of EFTA’s definition of injury, even though she did receive a form of notice; (2) a Rule 68 offer of proof to her – precertification – did not moot her claim; and (3) EFTA’s amendments did not fall within the exception to the general presumption against statutory retroactivity. A dissent took issue with the standing holding as “respectfuly, silly stuff,” reasoning: “Mabary cannot show that she suffered a cognizable injury in fact, so she can sue only if the existence of her statutory cause of action sufficed to satisfy Article III.”

TM machine. While she received an on-screen notice about a $2.00 fee, the machine did not have a posted external notice about the fee — a violation of the Electronic Funds Transfer Act at the time. After amendments to the EFTA that eliminated the Bank’s liability (if applicable), the district court dismissed Mabary’s claim and denied certification of a related class. Mabary v. Home Town Bank, N.A., No. 13-20211 (Nov. 5, 2014). The Fifth Circuit reversed, holding: (1) Mabary had Article III standing as a result of EFTA’s definition of injury, even though she did receive a form of notice; (2) a Rule 68 offer of proof to her – precertification – did not moot her claim; and (3) EFTA’s amendments did not fall within the exception to the general presumption against statutory retroactivity. A dissent took issue with the standing holding as “respectfuly, silly stuff,” reasoning: “Mabary cannot show that she suffered a cognizable injury in fact, so she can sue only if the existence of her statutory cause of action sufficed to satisfy Article III.”

The Baptists bought a home insurance policy from Nationwide in 2006. In 2008, they lost their home to foreclosure. They remained in the house, however, until December 2011 — before a court-ordered eviction date of January 13, 2012, but after fire did serious damage to the house in December. They made a claim on the Nationwide policy, which discovered that they no longer owned the house as part of its post-loss investigation. Nationwide Mut. Ins. Co. v. Baptist, No. 13-60726 (Aug. 7, 2014). While Nationwide won a summary judgment about coverage on the ground that the Baptists no longer had an insurable interest by the time of the fire, the Fifth Circuit affirmed because the Baptists’ “renewals of their policy constituted their affirmations to Nationwide of their initial application for insurance, material portions of which were no longer true.” Those misstatements allowed Nationwide to rescind the policy under Mississippi law.

The Leas joined a wholesale membership club, and made a $100 payment that day as part of the down payment. Their contract did not include the starting date, interval, or date of the month when their installment payments would be due over the next 3 years for the $4,000 membership fee. Lea v. Buy Direct LLC, No. 13-20281 (June 12, 2014). The Fifth Circuit found that TILA applied because the Leas had entered a credit transaction, even if they had not bought any goods yet. Then, recognizing that “[Defendant’s] decision to leave the contract blanks unfilled was, at least in part, an accomodation to the Leas,” the Court nevertheless reversed the district court’s summary judgment for the club on the Leas’ TILA claim. “Perhaps our reversal falls into the category of letting no good deed go unpunished. Another perspective, though, is that TILA provides an unvarying set of rules that protect consumers who might otherwise voluntarily waive what they should not.” Thus, although “[w]e do not perceive any harm here . . . harm is not a prerequisite for [TILA] relief.”

Two cases warn against skipping foundational steps (or “not showing your work”):

1. The dismissal of Garcia v. Jenkins Babb, LLP was affirmed for failure to allege facts sufficient under Iqbal to show that an FDCPA claim arose from a consumer transaction; more specifically, “giv[ing] no indication what item was purchased or what service was paid for, much less explain how the item or service was intended for personal or family use.” No. 13-10886 (May 29, 2014, unpublished). (The case returned, and dismissal was again affirmed, in Israel v. Primary Financial Services, No. 14-10012 (May 28, 2015, unpublished)).

2. An award of sanctions was reversed and remanded in Arnold v. Fannie Mae when “the

district court abused its discretion by failing to adequately articulate the authority, the basis, and the reasoning for the sanctions” under Rule 11, inherent power, or 28 U.S.C. § 1927.

In the recent case of French v. EMC Mortgage Corp., No. 13-50417 (April 29, 2014, unpublished), these allegations were deemed to “reference[] the FDCPA by way of asserting a cause of action under this federal statute,” and thus allowing removal:

“V. ILLEGAL MORTGAGE SERVICING AND DEBT COLLECTION PRACTICES.

. . .

Specifically in collection calls and notices, monthly statements, payoff statements, foreclosure notices, and otherwise, EMC routinely makes misrepresentations to borrowers about their loans, including: [6 topics]

. . .

Plaintiffs submit that Defendant EMC’s conduct in this matter is in direct violation of the Texas Fair Debt Collection Practices Act, the Federal Fair Debt Collection Practices Act and the above referenced stipulated injunction.”

This case rested on Howery v. Allstate Ins. Co., 243 F.3d 912 (5th Cir. 2001), in which the following allegations did not create federal question jurisdiction, because “[f]rom its context, it appears that Howery’s mention of federal law merely served to describe types of conduct that violated the DTPA, not to allege a separate cause of action under the FCRA”:

The acts, omissions, and other wrongful conduct of Allstate complained of in this petition constituted unconscionable conduct or unconscionable course of conduct, and false, misleading, or deceptive acts or practices. As such, Allstate violated the Texas Deceptive Trade Practices Act, Sections 17.46, et seq., and the Texas Insurance Code, including articles 21.21, 21.21-1, 21.55, and the rules and regulations promulgated thereunder, specifically including 28 TAC Section 21.3, et seq. and 21.203.

…

Allstate’s destruction of [Howery’s] file … constituted a further violation of the Texas Deceptive Trade Practices Act, for which plaintiff sues for recovery. Allstate also engaged in conduct in violation of the Federal Trade Commission rules, regulations, and statutes by obtaining Plaintiff’s credit report in a prohibited manner, a further violation of the Texas Deceptive Trade Practices Act….

While these holdings are consistent, the line between them is only a few words in a lengthy pleading. They underscore the importance of detail in considering whether removal is appropriate.

Congress amended the Fair Credit Reporting Act to have a limitations period of “2 years after the date of discovery by the plaintiff of the violation that is the basis for such liability.” The plaintiff in Mack v. Equable Ascent Financial, LLC argued that this amendment meant that “he could not have ‘discovered’ the violation until he had researched the statute.” No. 13-40128 (April 11, 2014). The Fifth Circuit disagreed, finding that the amendment was made to equalize the treatment of different types of claims, and that the plaintiff’s reading “would indefinitely extend the limitations period.”

Payne sued Progressive Financial for violations of fair debt collection statutes, seeking statutory damages, actual damages, attorneys fees, and costs. Payne v. Progressive Financial Services, No. 13-10381 (April 7, 2014). Progressive made a Rule 68 offer of $1,001 in damages and fees to the date of the offer, to which Payne did not respond. The district court reasoned that Payne had not pleaded a basis to recover actual damages, and that the unaccepted offer mooted her claim for statutory damages because it exceeded the amount she could recover. The Fifth Circuit reversed, finding that the district court’s analysis of the actual damages claim conflated jurisdiction with resolution of the merits; accordingly, Progressive’s offer was incomplete because it did not address actual damages. A footnote reminds that a complete Rule 68 offer can moot a case, and that the Court did not reach the argument that the offer was incomplete because it did not include post-offer fees and costs.

Mississippi brought six parens patriae actions alleging inappropriate charges for credit card “ancillary services” in violation of state law. Defendants removed under CAFA and on the ground of complete preemption, and the district court denied remand. Hood v. JP Morgan Chase & Co. (Dec. 2, 2013). The Fifth Circuit reversed. As to CAFA, it found that defendants (who have the burden) did not establish that any plaintiff had a claim of $75,000 – especially when Mississippi offered evidence that the average yearly charge at issue was around $100. The Court also observed that the defendants likely had similar information in their records. The Court acknowledged that federal usury laws have the effect of complete preemption, but found that the charges at issue in these cases could not be characterized as “interest” within the meaning of those laws.

Washington Mutual (“WaMu”) failed; Chase took over its mortgage operations from the FDIC. In the meantime, borrower Dixon (after receiving notice from Chase that it was replacing WaMu as mortgagee and servicer) obtained a default judgment in state court against WaMu for $2.8 million and a declaration that all liens were cancelled. A year later, Chase foreclosed on the property and obtained title at a foreclosure sale. Chase sued in federal court to quiet the cloud on title created by the recordation of the default judgment. JP Morgan Chase Bank NA v. Dixon, No. 12-40590 (Oct. 7, 2013, unpublished). The district court granted summary judgment to Chase. Dixon argued that this ruling violated the Rooker/Feldman doctrine about federal review of state court judgments. The Fifth Circuit disagreed, noting that the federal ruling did not technically “nullify” the state court judgment, and that Chase was not a party to the state proceedings and thus Rooker/Feldman was not implicated.

In Serna v. Law Office of Joseph Onwuteaka, P.C., the plaintiff alleged that a debt collector had sued him in an impermissible venue under the FDCPA . No. 12-20529 (Oct. 7, 2013). The defendants obtained summary judgment on limitations; the question was whether the offending act under the FDCPA — to “bring such action” — was filing of the suit or service. The Fifth Circuit found that the term “bring” is ambiguous in this context, which justifies consideration of the statute’s history and purpose. It then concluded that “the FDCPA’s remedial nature compels the conclusion that a violation includes both filing and notice,” and reversed. A dissent argued that the term was not ambiguous, since the term “brought” refers only to filing in another provision of the statute.

The Fifth Circuit affirmed the dismissal of several mortgage-related claims by a borrower against JP Morgan, based on the reasoning of the Court’s opinions in the area in 2013. Hudson v. JP Morgan Chase Bank NA, No. 13-50407 (Sept. 23, 2013, unpublished). After the district court ruled, the Bank of New York (who had been sued but not served) entered an appearance in the case, and asked the Fifth Circuit to dismiss the claims against it as well. Finding that BONY was not a party at the time of the district court’s dismissal ruling, the Court dismissed that request for lack of jurisdiction.

The FTC sued debt negotiation companies, claiming that their ads deceptively promised substantial reductions in consumers’ credit card debt. The district court concluded that “deception” under section 5 of the FTC Act should be evaluated on the basis of all information disclosed by the companies to consumers up to the point of purchase, and entered judgment for the defendants. FTC v. Financial Freedom Processing Inc. No. 12-10520 (Aug. 12, 2013, unpublished). The Fifth Circuit thought that the district court’s analysis was “dubious,” noting authority in other circuits that holds “each advertisement must stand on its own merits.” The FTC, however, elected to challenge the district court’s finding about deceptiveness at the point of purchase. Here, “while the Companies’ radio ads and websites may be misleading–indeed, it is difficult to conclude that the websites are not deceptive–we are satisfied that substantial evidence supports the district court’s finding . . . .”

After sidestepping an issue about the Rooker-Feldman doctrine in the context of mortgage servicing earlier this year, the Fifth Circuit revisited the topic in Truong v. Bank of America, 717 F.3d 377 (2013). After a review of the doctrine (“‘Reduced to its essence, the Rooker/Feldman doctrine holds that inferior federal courts do not have the power to modify or reverse state court judgments’ except when authorized by Congress.”), the Court found that it did not prevent a claim arising from alleged misconduct during the course of a foreclosure case. On the merits, however, the claim failed because of an exemption in Louisiana’s unfair trade practices act for “[a]ny federally insured financial institution,” and the Court affirmed dismissal on that basis.

Wagner v. BellSouth Telecommunications underscores a recent holding that a reduced credit rating is not enough to establish damage under the Fair Credit Reporting Act. 12-31080 (April 5, 2013, unpublished). The opinion also reminds that to recover mental anguish damages under the FCRA, a plaintiff must offer “evidence of genuine injury, such as the evidence of the injured party’s conduct and the observations of others,” and to demonstrate “a degree of specificity which may include corroborating testimony or medical or psychological evidence in support of the damage award.” (quoting Cousin v. Trans Union Corp., 246 F.3d 359, 371 (5th Cir. 2001)). The Court also reviewed basic limitations principles under the FCRA and its Louisiana state analog.

The borrowers in Priester v. JP Morgan Chase alleged two violations of the Texas Constitution about their home equity loan — not receiving notice of their rights 12 days before closing, and closing the loan in their home rather than the offices of a lender, attorney, or title company. 708 F.3d 667 (5th Cir. 2013). A cure letter was not answered and they sued for forfeiture of interest and principal under the state constitution. The Fifth Circuit affirmed the dismissal of the claim under the Texas 4-year “residual” limitations period, finding that was the prevailing view of courts that had examined the issue, and disagreeing with a district court that had found no limitations period. That court reasoned that a noncompliant home equity loan was void, but the Fifth Circuit concluded that the cure provision in the Constitution instead made it voidable. Tolling doctrines did not apply since it was readily apparent where the closing occurred. The Court also affirmed the denial of a motion for leave to amend to add new claims and non-diverse parties, reviewing the factors for both aspects of such a motion.

The plaintiff in Smith v. Santander Consumer USA received $20,43.59 in damages for violation of the Fair Credit Reporting Act. No. 12-50007 (Dec. 20, 2012). The Fifth Circuit agreed that damages were not recoverable solely for a reduced line of credit, but found sufficient other evidence about harm to the plaintiff’s business and personal finances to affirm. Enthusiasts of appellate arcana will find it interesting to compare the Court’s analysis of a general federal verdict under the Boeing standard with the Texas damages submissions required by Harris County v. Smith, 96 S.W.3d 230 (Tex. 2002) (applying Crown Life Ins. v. Casteel, 22 S.W.3d 378 (Tex. 2000)).

Vanderbilt Mortgage v. Flores, arising from a collection suit about the financing for a mobile home, involved a substantial recovery on counterclaims for wrongful debt collection and filing of a fraudulent lien. 692 F.3d 357 (5th Cir. 2012). The Fifth Circuit affirmed in part and reversed in part, finding: (1) the release of the debtors unambiguously reached only the lien and not the underlying debt (thereby mooting some counterclaims); (2) property owners in the position of these debtors did not have an ongoing duty, for limitations purposes, to check deed records; (3) Tex. Civ. Prac. & Rem Code chapter 12, about fraudulent liens, does not require actual damages before penalties may be awarded; (4) Chapter 12 does not violate the Excessive Fines Clause; and (5) personal jurisdiction over one defendant was appropriate, particularly given the confusion in its own records about its activities.